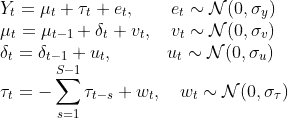

I'm relatively new to PYMC3 and I'm trying to implement a Bayesian Structure Time Series (BSTS) without regressors, for instance the model fit here in R. The model is as follows:

I can implement the local linear trend using a GaussianRandomWalk as follows:

delta = pymc3.GaussianRandomWalk('delta',mu=0,sd=1,shape=99)

mu = pymc3.GaussianRandomWalk('mu',mu=delta,sd=1,shape=100)

However, I'm at a loss for how to encode the seasonal variable (tau) in PYMC3. Do I need to roll a custom random walk class or is there some other trick?